Digital transformation is not a new topic. Since early 2013, it has been steadily gaining interest worldwide, as this ascending graph in Google Trends proves. It’s pretty safe to say now that we’re all fully adept at speaking about it and can even confess to including it or seeing it featured in most tech roadmaps for companies across many industries, for quite a few years now.

On the other side, the risk-averse mindset of the majority of end customers hasn’t exactly put pressure on banks to digitally transform their operations and adopt new technologies.

Nowadays, as most people work remotely – and this is, for many, the first time they do it – a new consumer behaviour is being shaped, one that values digital convenience, user experience, and adaptability.

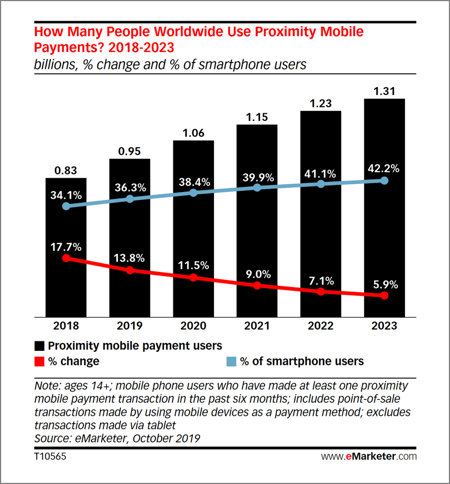

As per eMarketer’s pre-pandemic estimations, “in 2020, for the first time, more than 1 billion people worldwide will use a mobile payment app to pay in-store at least every six months”. This is an improvement in the rate of adoption but doesn’t say much about the frequency of mobile payments when we think that there are an estimated 3.5 billion smartphone users in the world. But how will the post-pandemic business landscape accelerate this vision and deliver it to day-to-day practice, in an industry so heavily regulated as Banking?

The rise of the Qualified Electronic Signature

Even though we’re in lockdown, our finances haven’t gone into a similar freeze period. However, we can’t easily go to the bank anymore to handle our accounts or manage our financial products.

This gives rise to new opportunities in adopting digital signature functionalities. There are already many options available but there has been a slow adherence to these new technologies as customers prefer to handle their finances in a branch rather than digitally, due mostly to a mindset more than to technology.

Digital signature will be the first chance we’ll see from banks who need to hit the ground running and offer the possibility to sign your financial documents remotely.

Digital onboarding gains traction as eCommerce reaches an all-time high

For eCommerce during the pandemic, it’s like Christmas – every day. With little to no alternative to shopping when entire countries go into lockdown and everyone is forced to stay indoors, spending time online and getting exposed to digital advertising, integrating digital onboarding within eCommerce flows is the most inspired solution.

At Encora, we’ve helped one of our customers, a medium-sized lender, to seamlessly integrate their loan origination fully digitally in the eCommerce flow of one of the largest retailers in Romania, allowing customers to minimize their time-to-yes for getting a personal unsecured loan to minutes rather than hours or days, without even leaving the website of the retailer.

This practice is happening now but we expect that it will gain even more traction as eCommerce surges during and post-pandemic.

Goodbye cash, farewell cards, hello mobile payments

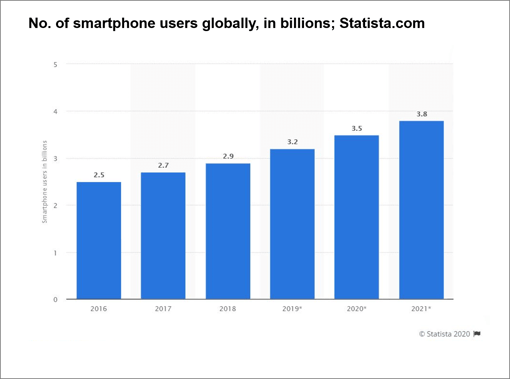

Apple Pay, Google Pay, Samsung Pay and so on – mobile payments have seen accelerated adoption worldwide, fueled by user-friendly wearable ecosystems and the prevalence of the smartphone. As per Statista estimations, there are already 3.5 billion smartphone users globally.

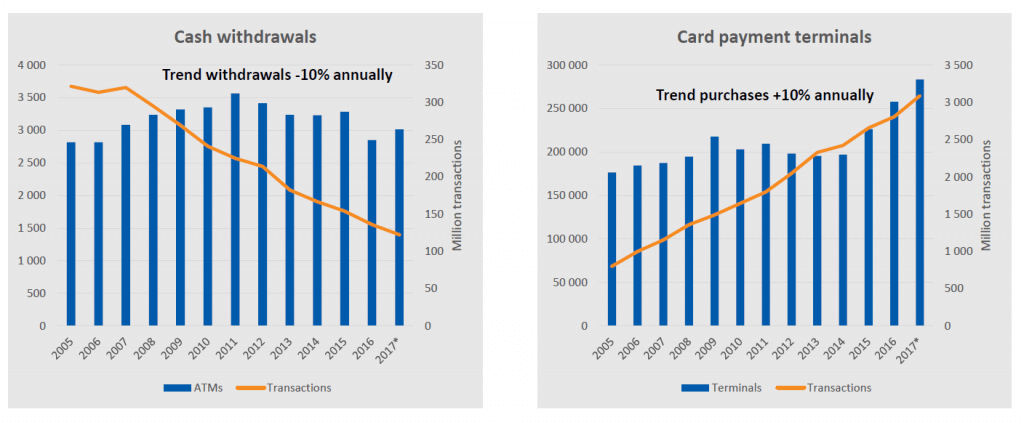

Bonus, going cashless with mobile payments is bad business for pickpockets. A long-time cashless country, Sweden, has seen a decrease in burglaries and high street beggars since adopting a nearly 100% cashless policy. Cash now amounts to only one per cent of the Gross Domestic Product (GDP) in Sweden as of 2019 data below (source: European Payments Council, the graphic below).

While during the COVID-19 pandemic, contactless payments are advised as a safety measure to avoid touching unsanitary banknotes, this is bound to accelerate the conversion of those members of society who for various reasons have been clinging on to their classic leather wallets to going all-in on mobile payments.

And once they’re be compelled by circumstance to give it a try, their reticence will very likely take a step back.

Conclusions

In an increasingly digital world, banks have access to all the technology they need to readily adapt to a new customer behaviour, shaped by the crisis of the coronavirus, but also by digital adoption in other areas about a modern lifestyle. The next step is to choose the right partner to deliver this vision quickly and efficiently

The driver of this accelerated digital transformation in banking is even stronger than regulation or technology: it’s a matter of delivering on the promise of a safe and efficient user experience to customers worldwide.

In addition to all this, regulation, too, will be forced to adapt so we’ll see more pressure from lawmakers to compel banks to offer 100% digital banking services to all customers as part of their standard offering.

The demise of the legacy systems and the shift to a truly digital experience that goes beyond the smoke and mirrors of an online front desk fueled by marketing tactics is just a matter of time, and COVID-19 may have just accelerated the rise of the digital bank.

Sources:

https://trends.google.com/trends/explore

https://www.europeanpaymentscouncil.eu/news-insights/insight/sweden-cashless-society-and-digital-transformation

https://www.statista.com/statistics/330695/number-of-smartphone-users-worldwide/